Key Takeaways

• 83% of election years since the S&P 500 began have historically provided positive performance.

• Value style investing has outperformed growth in the six months after every presidential election for the last 40 years.

• While the S&P 500 is at new highs, the Russell 2000 small cap index is still in a 20% drawdown – the largest we’ve ever seen with the S&P 500 at an all-time high. This has previously led to small cap outperformance and a joining with the S&P 500 at an all-time high.

There are many factors that influence stock market returns, but with a resounding win in Iowa a few weeks back and the latest Reuters poll putting Trump nearly 40% ahead of Haley in the battle for the Republican nomination, this week we consider what Trump’s possible return to the White House might mean for the S&P 500.

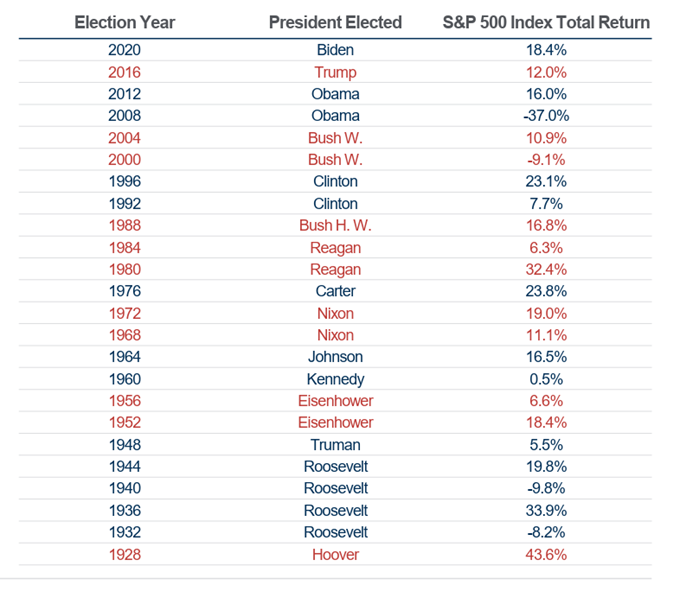

The good news for equity investors is that 83% of election years since the S&P 500 began have provided positive performance – regardless of which political party wins. History also tells us that the stock market prefers consistency in party, with an average return of 15% when a Democrat is in office and re-elected vs when a Democrat is in office and a Republican is elected returning 12.9%.

Historical US Presidential Election Results

Source: First Trust

In terms of investment style performance differential according to presidential elections, value names (where an investor believes that a company’s share price will recover within the investment horizon) have meaningfully outperformed their growth (where an investor believe the business revenue and earnings will grow) counterparts for six months after every presidential election for the last 40 years. See below for the historical total returns of the Russell 1000 Value Total Return Index and the Russell 1000 Growth Total Return Index over the past 11 elections.

Value vs. Growth: Performance Following Presidential Elections Since 1980

Source: First Trust

While the main spending policies between political parties, namely the Inflation Reduction Act (IRA) and the Creating Helpful Incentives to Produce Semiconductors and Science Act (CHIPS) will likely continue, the rhetoric around immigration and foreign support is currently dissimilar. It is prudent to also mention the geo-political volatility and global trading ramifications that may result from Trump’s potential return to the White House. For example, if Trump’s 10% tariff on all imported goods to the US comes into force – this would have a profound structural impact on global economic activity and broad negative implications for most asset classes.

Bowmore portfolios

A lot can happen between now and November, especially considering the four outstanding criminal charges against Trump and the series of trials that he will need to attend in the run up to election day, so our stance is to maintain our diversified exposure until the picture becomes clearer.

Portfolio allocations to US markets make up the largest regional exposure within portfolios when considering specific geographical equity funds with thematic exposure. Over the last three months, our sustainable large cap US exposure has proven beneficial, returning 16.11%, while our thematic exposure to the technology sector (84.04% of the fund is invested within US equities) has returned 18.52%. We also took the decision in November last year to increase US small and mid-cap value style exposure within our core mandate, and since purchased, the fund has returned 7.60%.