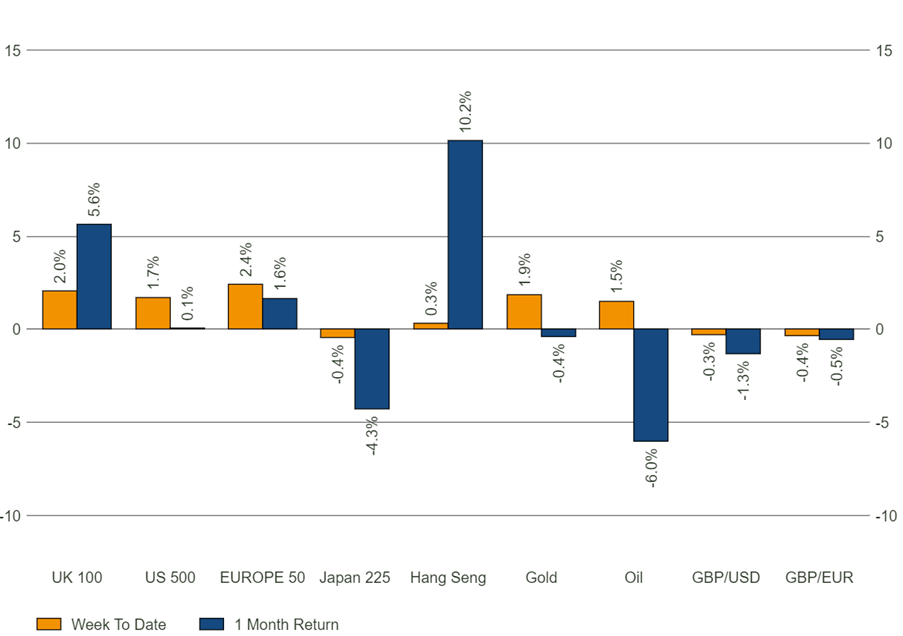

- Aside from the US, other major markets trade below their long-term average

- UK equity funds have been unpopular amongst investors and have seen 35 months of consecutive outflows

- With the European Central Bank poised to cut interest rates in the coming months, this could boost popularly of the region

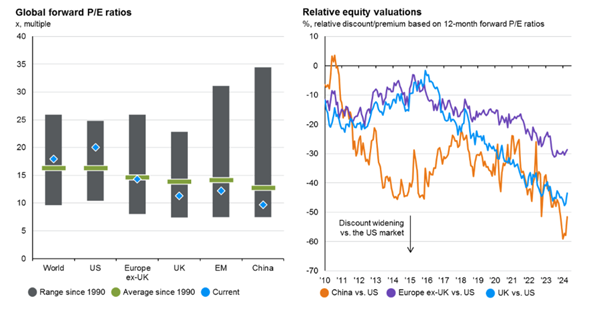

Having recently explored the general valuation gap between small and large cap stocks, this week we are looking into the difference in valuations between stocks listed in Europe or the UK and those listed in the US. It is no secret that the US market is running hot at the moment – it is currently trading at a forward P/E of 20.1x, well above its long-term average of 16.3x. Meanwhile, Europe is trading at a multiple of 14.3x (average of 14.6x) and the UK is down at 11.3x (average of 13.9x). So not only does the US typically trade at a premium to the rest of the world, but it is also expensive relative to itself – while the UK and Europe are cheap, even by their own standards. The charts below show the regional equity valuations relative to their own average (LHS) and emphasise the increasing gap in valuations (RHS).

Source: JP Morgan

This valuation gap is starting to have serious implications on the UK Stock market. April was the 35th consecutive month of outflows from UK equity funds despite UK investors adding £1.9bn to equity funds in the month. This is creating a vicious cycle where the more UK stocks underperform relatively, the more outflows it sees, and the worse it does. Boards have a fiduciary duty to act in shareholders’ best interests and that has resulted in UK companies moving their listings to the US to benefit from more favourable share pricing. Ferguson, a British plumbing and heating distributor moved its primary listing to the NYSE in 2022. Arm, a British semiconductor company chose to IPO on the Nasdaq last year instead of London. Even Shell, the second largest constituent of the FTSE 100, has been talking about moving their listing to New York recently.

Are the Valuations Justified?

Part of the valuation gap stems from the type of companies that you would find on each stock market. The FTSE 100 is famed for having a ‘value’ style tilt where you will find mostly banks, oil giants, miners and healthcare companies. The European stock market is not dissimilar in its nature with it being dominated by consumer discretionary companies like LVMH or consumer staples like Nestlé.

None of these companies scream revenue and earnings growth like the US’ tech bias, (think Amazon, Tesla, Nvidia, Meta) and this is reflected in the numbers. Profit margins in the US are higher on average at about 12% for the S&P 500 vs 10% for MSCI Europe and the FTSE All-Share. Earnings per share (EPS) growth estimates are almost 10% for US stocks and less than 5% for their European and UK counterparts. Investors are willing to pay a premium for companies with greater growth potential and there is evidence that you will find more of those companies listed in the US.

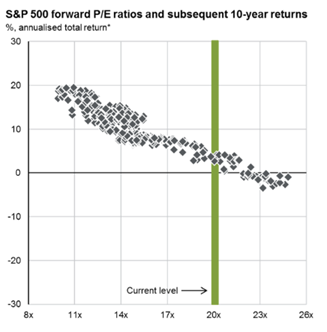

However, a great company at a bad price is still a bad investment. As I said previously, the US is running hot, and the expected annualised returns based on the current level of valuations is a low single digit figure:

Source: JP Morgan

Mean reversion theory suggests that an asset’s price will eventually return to its long-term average. This implies that the US market has potential to contract a significant amount just to be ‘fair value’ relative to its own history, whereas the UK market would benefit from a 23% uplift just getting back to ‘fair value’.

Bowmore Portfolios

We don’t know what is going to be the catalyst that triggers a reversion in valuations for these unloved markets but the recent success stories of companies like Novo Nordisk and ASML in Europe showcase the quality that is on offer and give us confidence that it is ‘when’ not ‘if’. 60-75% of trading in US and European markets is algorithmic meaning it only takes a little momentum in one direction for the tide to turn quite significantly. This month, we will introduce two new European equity funds into portfolios, repositioning our exposure to benefit from regional growth momentum.