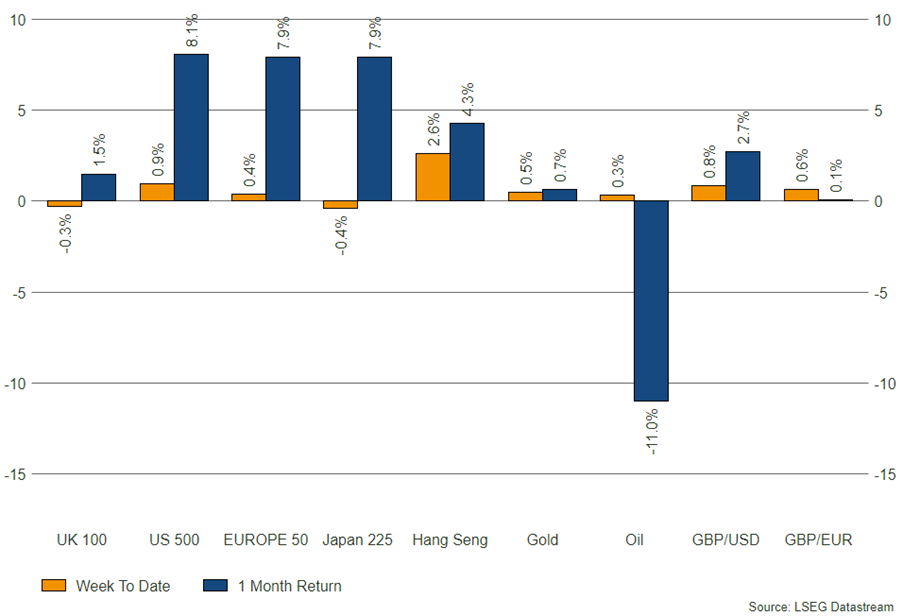

Key takeaways

- Jeremy Hunt delivers tax cuts in Autumn Statement through national insurance reform.

- Conservative support increases on back of cuts, though remains some way behind Labour.

- UK growth to be 0.6% for 2023, according to the Office for Budget Responsibility.

The Autumn Statement

After US markets were on holiday last Thursday for thanksgiving, the British people have had a couple of days to digest Chancellor of the Exchequer, Jeremy Hunt’s Autumn Statement and what it means for them. With an overhaul for national insurance, a revision to the living wage and a pension payment rise, many have accused Hunt of delivering a statement designed to placate the public ahead of the next general election.

Headline changes

- Main rate of national insurance (NI) cut from 12% to 10%, affecting 27 million people.

- Self-employed Class 2 NI abolished and Class 4 cut from 9% to 8%.

- Living wage increased to £11.44 per hour.

- State pension payments to increase by 8.5%, in line with wages.

- Business rates 75% discount extended for a year.

Outlook

Whilst the date for the next election is yet to be set, headline changes such as the 2% cut to national insurance appear to have gone down well with the public. Rishi Sunak’s Conservative government’s backing rose 4 percentage points in a YouGov poll, though this still came in 19 points behind Labour.

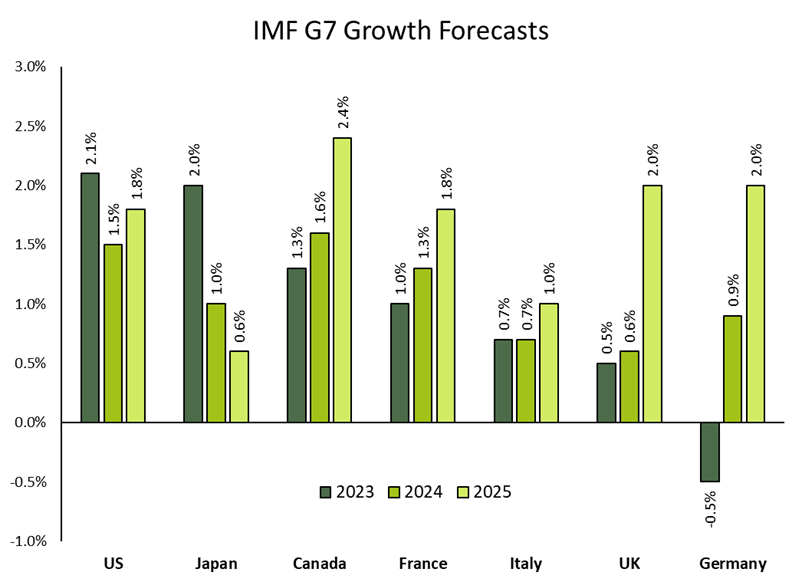

Aside from public opinion, UK growth and inflation figures were released by the Office for Budget Responsibility. It is expected that the UK economy will grow by 0.6% this year, and 0.7% next, with inflation to fall to 2.8% by the end of next year. These growth numbers came in slightly more optimistic than those of the International Monetary Fund (IMF), which sees the UK growing the second slowest of the G7 nations in 2023, ahead of only Germany.

Source: imf.org

Bowmore portfolios

Though domestic policy and growth is of course meaningful to those of us residing in the UK, global markets are less affected by the economic trends set by the UK when compared to the likes of the US, China or even Europe. As such, our diversified portfolio of assets will help spread the risk should growth in the UK suffer further, with our government bond allocations providing protection in a downturn. On the flipside, our allocation to equities across the UK market is well positioned to benefit should momentum in domestic risk assets build, with valuations at depressed levels when compared to global peers.