Key Takeaways

• US inflation falls to 3.0% year on year

• Core inflation is also slowing, with the lowest monthly reading in two years

• The tight labour market is still putting pressure on the Federal Reserve to raise rates

After two years of elevated inflation, June’s month-on-month increase in US core inflation (headline inflation excluding volatile components such as food and energy) was 0.16%; its slowest rise in more than two years. Headline US inflation continued its decline, with the consumer-price index registering a 3.0% year-on-year rise in June; a significant slowdown from the 9.1% seen in June 2022.

Some may argue that after the Federal Reserve (Fed) held interest rates steady last month, these softer inflation readings will prompt them to continue a more accommodative path in next weeks meeting. However, inflation readings are not the only indicator available to the Fed, and the labour market provides a different lens.

The US labour market

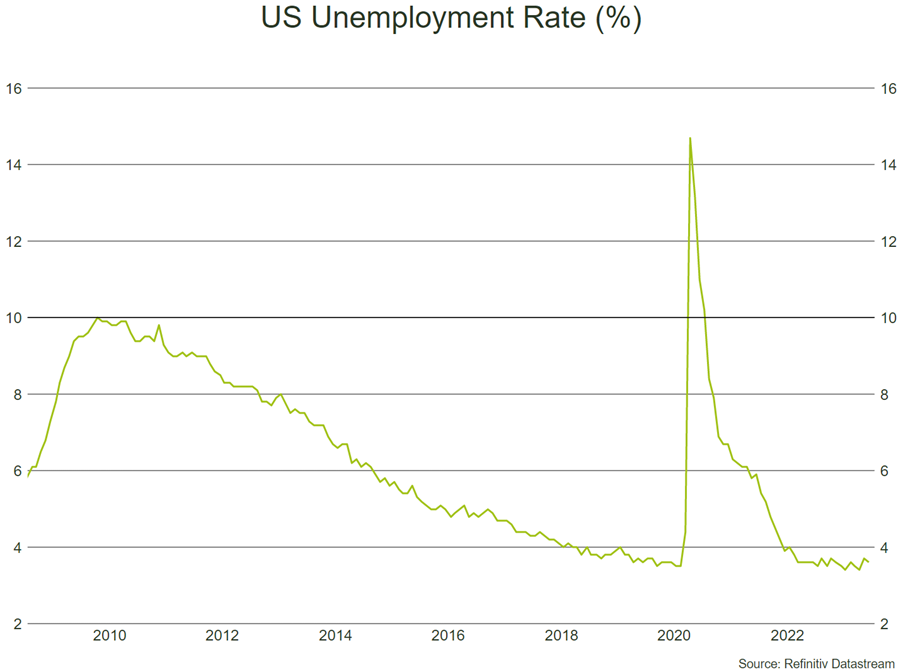

US unemployment remains close to all-time lows, with 3.6% of the labour force out of work. Despite this, for every unemployed person in the US there are more than 1.5 jobs available, according to the Bureau of Labour Statistics. A ratio which has come down since its peak in mid-2022, but well above its historical range, which is below one. Since Covid, the US economy has created c.4 million jobs, putting employment way above its long-term trend.

Source: Refinitiv

A persistently tight labour market has allowed the Fed to be more aggressive in its interest rate policy, and with numbers continuing to hold up, it is widely expected the Fed will raise rates to 5.5% later this month. An argument to support this move is that wage growth in the US, thanks to the tight labour market, was 5.7% for May, year on year. Wage growth is inflationary and has helped support consumer sentiment, with spending back on trend after dipping in Covid, and despite higher inflation.

Looking forward

With some assigning a 92% probability that the Fed will hike this month, the real question is what the US central bank will do after its July meeting. Jerome Powell, chair of the Fed has said that they are inclined to implement additional rate rises before the end of the year, but that the level of these rises and their frequency will be less predictable. This indicates that the Fed is perhaps more willing to be led by the data, than an all-out attack on demand-driven inflation, and that rates are close to their peak in the US.

Bowmore portfolios

Peak rates in the US will be an inflection point for markets. When we do start to see interest rates fall, this will be a positive driver of sentiment in risk assets and will be supportive for growth. Although we have recently taken some profits from our broad US equity index allocation, we remain diversified, with a healthy allocation to global and US equities that will benefit from softer monetary policy when it arrives.

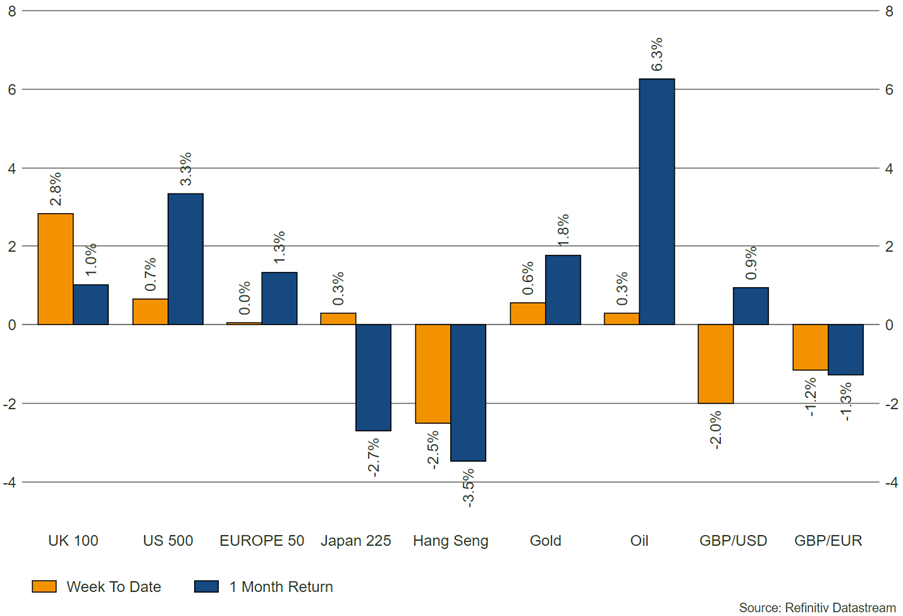

Source: Refinitiv – Market returns as at 20/07/2023