Key takeaways

- Inflation and interest rates have lifted bond yields.

- Investment flows into bonds and money markets rising with higher return profile.

- Bond issuance falling since 2021 due to tighter credit market.

Bonds are back

After a decade of bond yields not being far off zero in the majority of developed markets, and even falling into negative territory in Germany and Japan, fixed income is back. As we have previously written, rising inflation has encouraged tighter monetary policy around the globe, lifting yields to levels not seen since the financial crisis of 2008. The actions taken by the majority of central banks, led by the US, has enhanced the attractiveness of fixed interest assets.

Inflows

As a result, investors are reacting. In Europe, asset managers are seeing a rise in clients moving away from some equities and pure cash holdings to money market and bond funds, with the latter seeing c.€64 billion of inflows in the first four months of the year. Investors are taking advantage of higher returns available at the shorter end of the yield curve (bonds that mature over the next few years, which are yielding higher than their longer-term counterparts).

The appetite for fixed income has definitely changed since the resurgence of inflation and we have seen interest rates rise. As above, the asset allocation of institutional and retail investors is adjusting. However, we have also seen a shift in the appetite to raise debt.

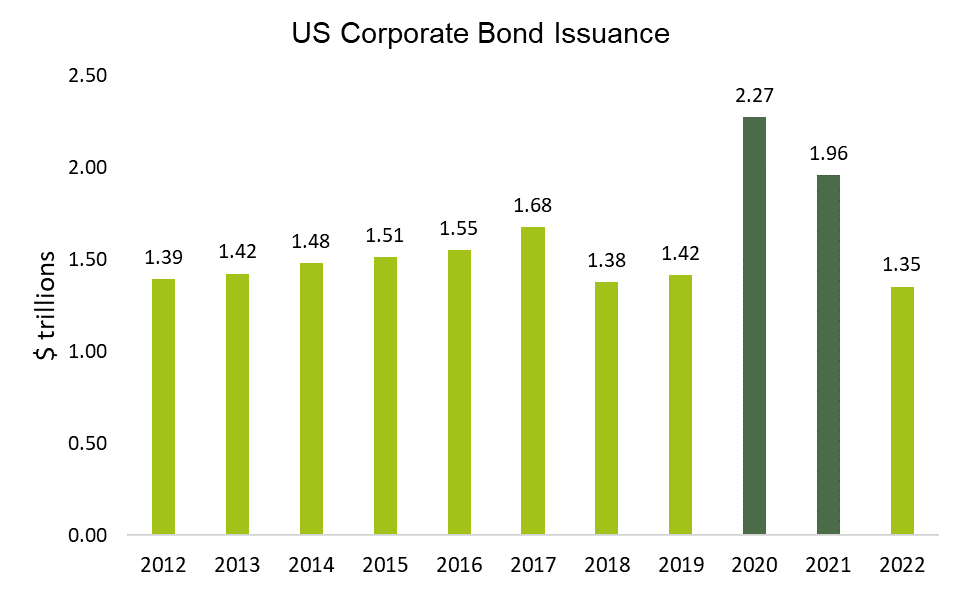

As yields pushed higher in 2022, and government programmes have pulled away from supporting bond markets, the appetite for bond issuance is coming back to more normal levels from peaks in 2020 and 2021. During these two years, US corporations issued over $4 trillion of debt as they took advantage of the macro-economic environment to raise cheap cash. That number fell to $1.4 trillion in 2022, reflecting the higher interest rate and yield environment.

Source: sifma.org

Bowmore Portfolios

With interest rate policy reaching its inflection point and investors anticipating peak rates this year, markets will start to price in the prospect of falling rates next year and a looser monetary environment. Though there have been no promises from the Federal Reserve, it is in the interest of economic growth to bring rates down. Should we see recessionary pressures build further, this will be food for thought for policymakers.

As and when rates fall, we will see yields retreat and capital values improve, with shorter dated bond yields likely to fall further than long-term yields, as these have been elevated higher. Within portfolios we invest in short dated high yield bonds, which have returned 3.7% for us this year, and remain an attractive prospect.

Source: Refinitiv – Market returns as at 03/08/2023