Key takeaways

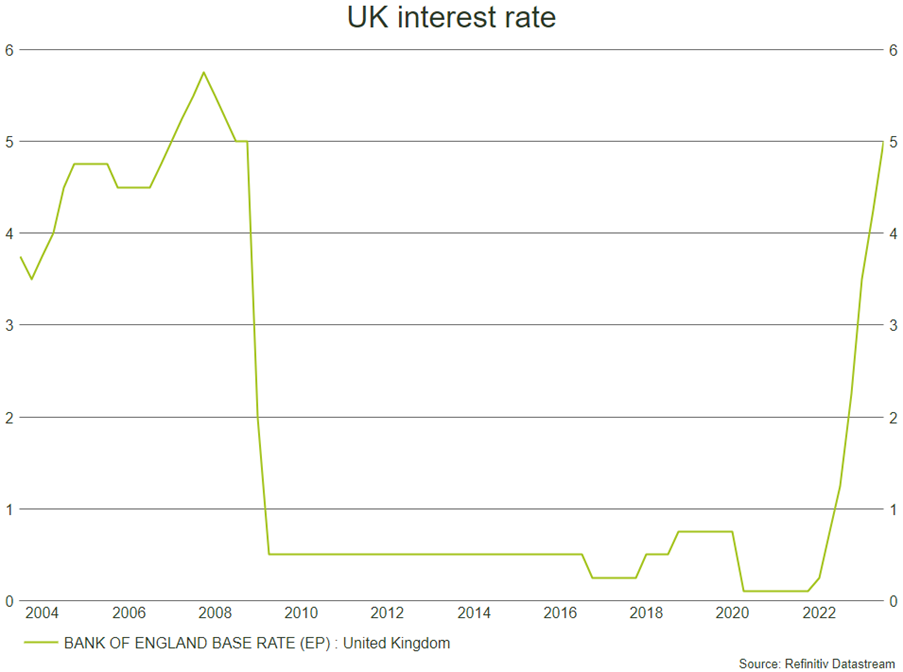

- Bank of England raises interest rate by 0.5% to 5.0%

- Core inflation higher in the UK at 7.1% in May

- Mortgage payments now make up 45% of income

On Wednesday, the Bank of England (BOE) increased interest rates by half a percent to 5.0%, back to a level not seen since 2008. With most expecting a 0.25% rise, this larger hike surprised investors and commentators as the bank ramped up its efforts to tackle stubborn inflation. The Monetary Policy Committee voted 7-2 in favour of a 13th consecutive increase, a week after the US Federal Reserve held rates steady for the first time since it started its hiking cycle.

Source: Refinitiv

Two members of the committee preferred to vote against the rise, arguing that it “would bring forward the point at which recent rate increases would need to be reversed” due to recessionary pressures. The BOE expects a mild recession this year in the UK, with GDP to contract by 0.7% for the 4th quarter of the year, compared to the last quarter of 2022.

The rate rise is a clear sign that the UK government and central bank believe inflation is still too persistent and action must be taken. Core inflation, which strips out volatile food and energy prices, rose again during the month of May to 7.1% from 6.8% the previous month; its highest level since 1992.

Market reaction

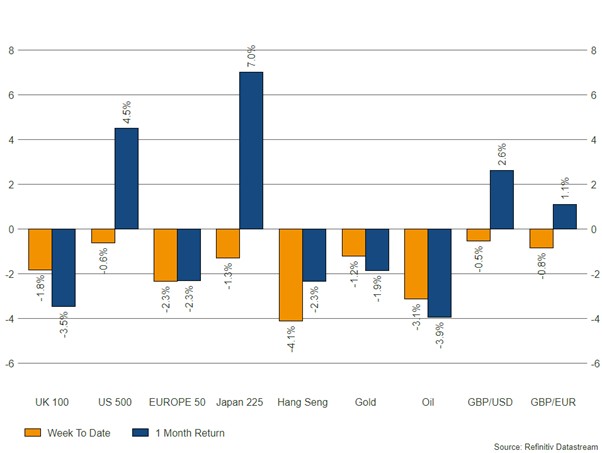

Whilst the hike came in higher than expected, UK markets were relatively muted on Wednesday. The pound rose slightly against the US dollar, before settling back around 1.27. Two-year UK government bond yields rose to 5.04%, whilst 10-year yields fell back to 4.40%, reflecting expectations of lower long-term rates. UK equity indices were relatively flat on Wednesday, though further losses were registered yesterday and today. UK large companies have fallen 1.1% since Tuesday, with the wider UK market down 1.4% at time of writing.

House prices

The average rate for a two-year mortgage has now hit 6.4%, and the UK Prime Minister, Rishi Sunak, has warned homeowners will face a “serious shock”. The Institute of Fiscal Studies said 1.4 million homeowners will see a fifth of their disposable income completely wiped out by rising mortgage rates, meanwhile the trade body UK Finance said it expects 98,000 to fall behind on payments this year.

As a comparison, in 1980 when rates were at 17%, the average UK house price was around £21,000 and mortgage costs accounted for 11.3% of income. Today, the average price of a house stands at £292,000, with mortgages eating up 45.2% of income.

Some lenders, such as Leeds Building Society, have confirmed they will not be passing on the rate rise to borrowers.

Bowmore portfolios

Last week we wrote about the opportunities we feel exist in the UK gilt markets, and this most recent interest rate rise does not change our view. Yields remain attractive, with a spread of maturities offering diversification, as we saw in bond markets on Wednesday as the two- and ten-year yields diverged. Should BOE expectations of a mild recession prove correct, an allocation to gilts will provide a defensive layer for portfolios.

Source: Refinitiv – Market returns as at 22/06/2023