- UK inflation returned to its 2% target this week, for the first time since July 2021

- Despite this, the BoE’s monetary policy committee (MPC) voted 7-2 to maintain the 16 year high 5.25% base rate on Thursday of this week

- The UK’s inflation has fallen faster than the EU and US, where the latest readings were 2.6% and 3.3% respectively

With the UK general election campaigns in full swing and services inflation remaining high (only falling 0.2% in May to 5.7%), it was in line with expectations that the MPC would maintain the base rate of 5.25% at this week’s meeting, despite CPI falling to its 2% target.

Nonetheless, the meeting gave reason for optimism around an August rate decrease, since two of the nine policymakers indeed voted for a cut and for “some” of the other seven MPC members (who voted to leave rates unchanged) say that the June decision was a “finely balanced” one.

In response to the published minutes, the market is now predicting a 0.25% rate decrease in August (with c.55% certainty). Bond yields and sterling fell both against the USD on Thursday in anticipation. Across the pond, it is expected that the Fed will begin to lower rates in September.

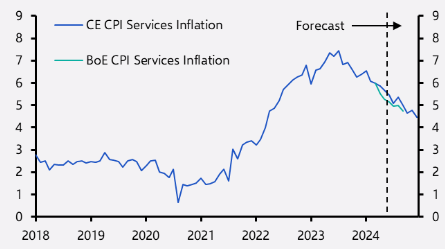

Services inflation

The latest ONS data confirmed that services price inflation – which the BoE believes gives a better indication of near-term inflation risk – cooled last month (but at a lower rate than expected, missing expectations by 0.4%) but remains elevated. The higher-than-expected reading is likely reflective of a 9.8% rise in the national minimum wage (now at £11.44 per hour) that came into force from 1st April of this year as well as indexed increases that take place annually. The wage increase was most evident in sectors with a meaningful proportion of minimum paid workers, for example restaurants and hotels inflation headed upwards from 5.8% to 6.0% while cultural services (concerts, cinemas etc.) inflation increased from 5.4% to 8.3%.

Private-sector wage growth is also running high – nearly double the rate that the BoE typically judge to be compatible with the 2% inflation target. Nevertheless, the stubborn services inflation indicates that businesses retain pricing power, and are able to pass on their cost increases to consumers.

Services CPI Inflation

Source: Capital Economics

Is policy change imminent?

Another factor that may have influenced the BoE’s decision is their expectation of inflation rising over the 2% target in the second half of this year by some 0.5% as the energy price cut of last year falls out of the annualised reading.

There are clearly multiple factors at play, and while a cut would seem more accessible at the next policy meeting in August, interest rates may not fall as quickly as the market predicted. Unease over the tightness of the labour market and the recently resurging strength in consumer demand could mean “spare capacity in the economy might open up to a lesser degree”, thereby placing less ongoing downward pressure on inflation.

As ever, the MPC have attested to their independence – noting that the upcoming election has no bearing on their decision-making process.

Bowmore portfolios

Having fallen out of favour, the UK has been victim to eight years of continuous outflows. Despite this however – we continue to see a sound investment opportunity within our domestic market and hold a meaningful actively managed allocation across portfolios as we expect an interest rate cut, when it comes, to be broadly beneficial for UK markets.

Our largest exposure is via the Artemis UK Select fund, an all-cap strategy that’s taken advantage of the rotation from growth to value style investing and balance sheet intensive businesses re-rating from exceptionally low levels, whilst higher rated capital light businesses are de-rating. We continue to believe this strategy has further to run, already returning 14.7% year to date.