Key takeaways

• Developed markets’ reliance on emerging economies and Asia falling due to Covid and geopolitical tensions.

• Chinese annual GDP growth comes in at 6.3% for Q2.

• Asian equities up 6.5% year-to-date in local currency terms.

Asian prospects

With protectionism on the rise over the last eight years, championed by Donald Trump during his presidency in the US, many have touted the end of globalisation. Geopolitical tensions have also eroded prior trade and collaboration between economic superpowers, with the Russia/Ukraine conflict and US/China relations encouraging the diversification of supply chains such as energy, tech and manufacturing. One consideration, therefore, is the health of many Asian economies, for which globalisation and worldwide trade have been a driver of growth, especially in emerging countries.

Deglobalisation?

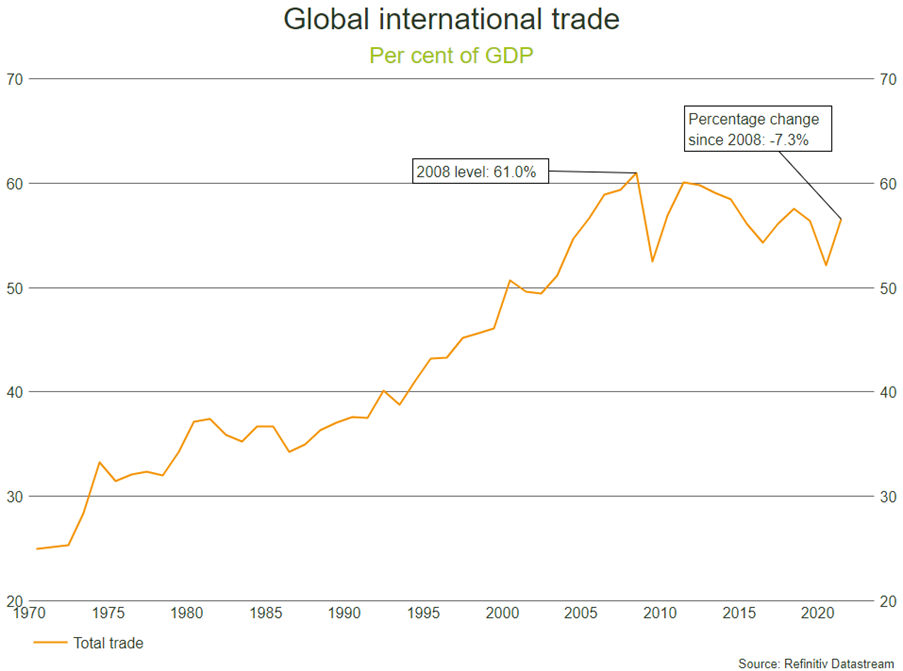

It is true that international trade as a percentage of GDP has dropped since its peak in 2008, before the global financial crisis. It is also true that a recent driver of this fall was Covid, in 2020, where global growth shut down.

Source: Refinitiv

Since the pandemic, many developed countries have worked to move jobs back into their own economies, with a view to be more self-reliant and kick-start growth after the 2020 contraction. More than 200,000 jobs moved back to the US from abroad in 2022, mitigating some of the risk of international supply chains, which saw ongoing stress when the likes of China remained in lockdown as the rest of the world opened up post-Covid. Russia’s invasion of Ukraine has enhanced this trend, pushing the likes of the UK and Europe to find alternative energy sources and speed up the roll out of renewables.

The impact on Asia

A less interconnected trade network will have its impact on Asian growth, but it’s not all bad news. Although the latest GDP figures released for China came in lower than expected, momentum is building after lockdowns were ended last year, and we are now seeing mid-single digit growth in the region. The Chinese economy grew by more than 6% in the second quarter year-on-year, showing steady improvement from the 2.9% registered last December. India’s growth sits in a similar range.

There are certain sectors in China that dominate global supply, such as semi-conductors, that will take time for developed nations to diversify. Even as the US is encouraging foreign manufacturers set up in China to add a second geographical hub (“China+1”, in the interest of lowering reliance on China) the likes of Vietnam and India benefit as likely destinations for new bases.

The development of its economies means that Asian countries can trade with each other, as well as more developed nations, and generate growth with less of a reliance on the west. Capital flows within Asia grew 23% in 2021 and as the region continues to grow, the importance of these economies in financial markets and investment portfolios will play a bigger role.

Bowmore portfolios

Year to date, the broad Asian market is up 6.5% in local currency terms, with our Indian equity exposure up c.5.4% over the same period, in sterling terms. Whilst allocating to the region can increase short term volatility, we can benefit from different drivers by diversifying our exposure with the likes of Asian markets. For example, when the US dollar weakens, or oil prices fall, these can provide a tailwind.

Source: Refinitiv – Market returns as at 27/07/2023