Key Takeways

• Germany was the worst-performing major economy of 2023 and economic activity has flatlined since early 2022 according to the IMF.

• Though, like other European stock markets this year, the DAX appears notably strong – returning 1.3% so far and 20.31% in 2023.

• With a significant string of earning expectation downgrades in the region, we expect fortunes for the DAX to be reversed this year.

Despite enjoying strong historical economic performance, Germany is currently ranked 36th out of the 44 European countries in terms of GDP annual growth with a current rate of -0.2%. This lack of growth is largely attributable to elevated energy prices (70% higher than before 2020), waning export business and industrial production as well as ongoing nationwide disruption due to striking workforces and protests.

There seems to be a perfect storm of multiple crises though this has not (yet!) translated to a poor stock market return. Notwithstanding each of the above-mentioned factors, bullish investor sentiment and a reduced fear over energy shortages has pushed the DAX higher this year, returning 1.3% so far. A return that we believe has overvalued assets.

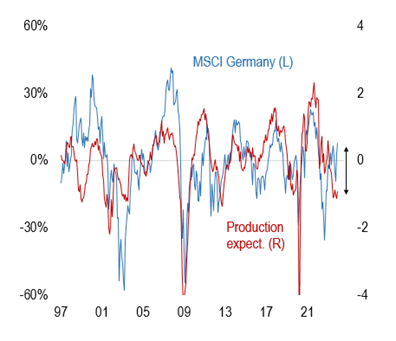

However, we consider this momentum unlikely to continue since the gap between production expectations and the German index has widened, as shown in the graph below. When similar gaps have formed previously, we have seen corrections of c.10% over the following year – a stark comparison to the average annual gains of 6.5%. Further, the ‘old economy’ make-up of the German stock market makes it particularly vulnerable to a manufacturing downturn since 31% of the index is comprised of industrials and car manufacturers that are heavily reliant on sales within the EU and US.

MSCI Germany vs, production expectations

Source: Numera Analytics, 2024

Why is Germany struggling?

1. The global economy: Recent trade tensions and geopolitical uncertainty have reduced the demand of manufactured goods, and since the German economy is heavily reliant on exports, this will negatively affect growth prospects.

2. Global reliance: Ongoing disruption in supply chains has weighed heavily on manufacturing productivity.

3. Competition from electric vehicles: The automotive industry faces stiff competition from electric car making rivals and that coupled with global semiconductor shortages has affected the profitability of a large part of the German index.

4. Transition target: Ambitious plans to increase the production of green energy within the region has presented short-term challenges as businesses within the energy sector are required to restructure.

5. Inflationary pressures: Consumer spending patterns are heavily influenced by inflation and increased prices can translate into reduced spending and therefore growth.

6. Geographical influence: Germany’s economic performance is closely tied to that of the broader Eurozone and can be affected by economic recovery challenges faced elsewhere in other EU countries.

Bowmore portfolios

We’ve long held an actively managed growth style European equity fund within the ESG mandate that while having a carbon footprint 80% lower than that of the MSCI Europe ex UK’s index and robust screening filters based on the UN’s Sustainable Development Goals, has returned 4.5% over the last month. The fund allocates across continental Europe to take advantage of sustainable trends and innovations including biotechnological advances within immunology, digitalisation and industrial diversity.