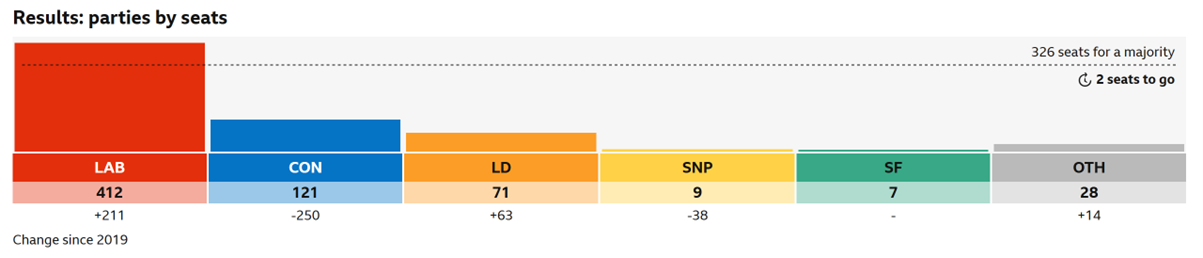

- The worst defeat for the Conservatives in 100 years in terms of seats and their lowest share of the vote ever

- The UK Government has limited fiscal headroom to spend given current debt levels – muting the impact on Equity and Bond markets

- Tax changes affecting Capital Gains Tax or Inheritance Tax could have longer term market implications but the short-term looks stable

It wouldn’t be right to talk about anything this week other than Labour’s landslide victory, although looking at the share of the votes, I’d argue it’s more of a Tory defeat than a Labour win. Labour only got about 1.5% more of the vote than they did in 2019 and actually 5% less than they did in 2017 under Corbyn. However, we are where we are and Labour have a majority. Some of the records broken this election show the country’s desire for change and economic stability. It was the worst defeat for the Conservatives in 100 years in terms of seats and their lowest share of the vote ever. The Lib Dems won the most amount of seats they’ve ever won as did the Green Party.

Source: BBC News

So what does this mean for markets?

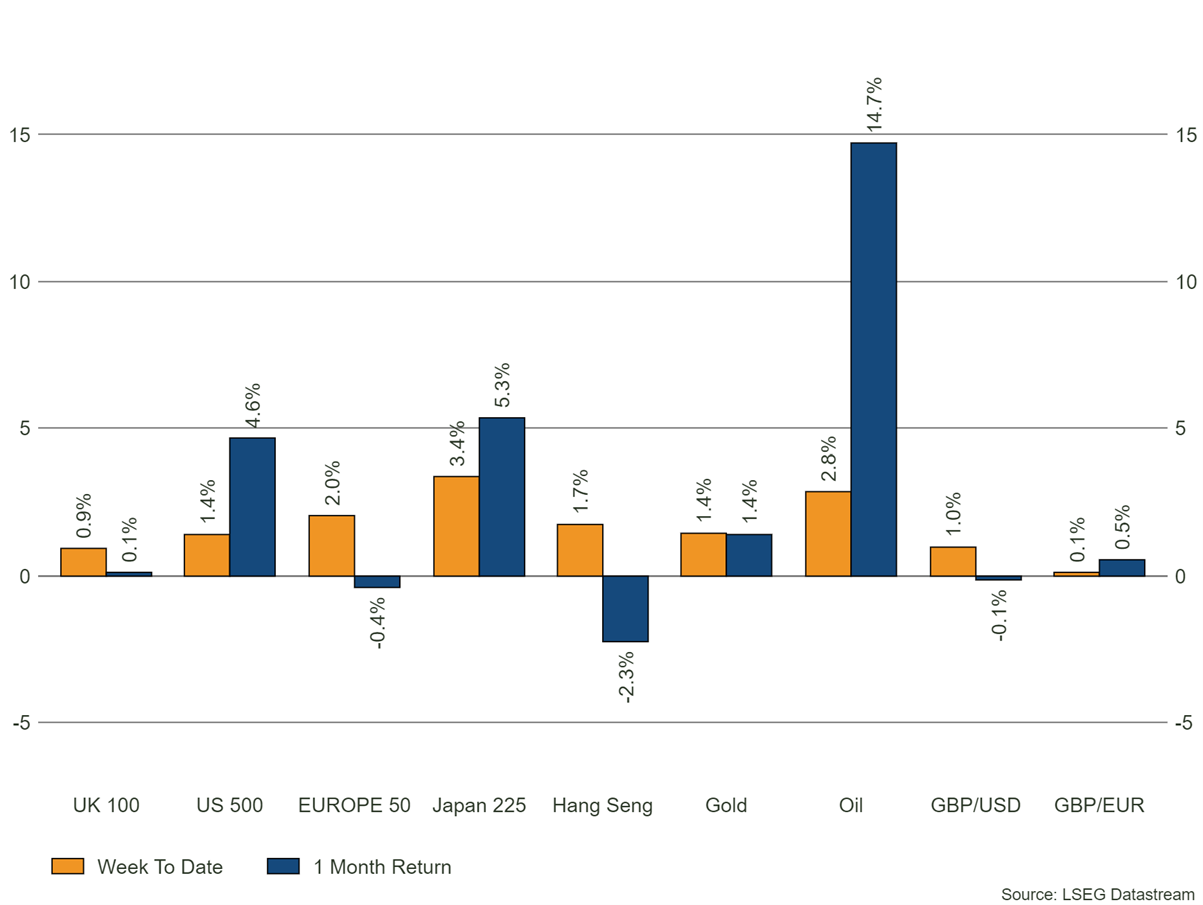

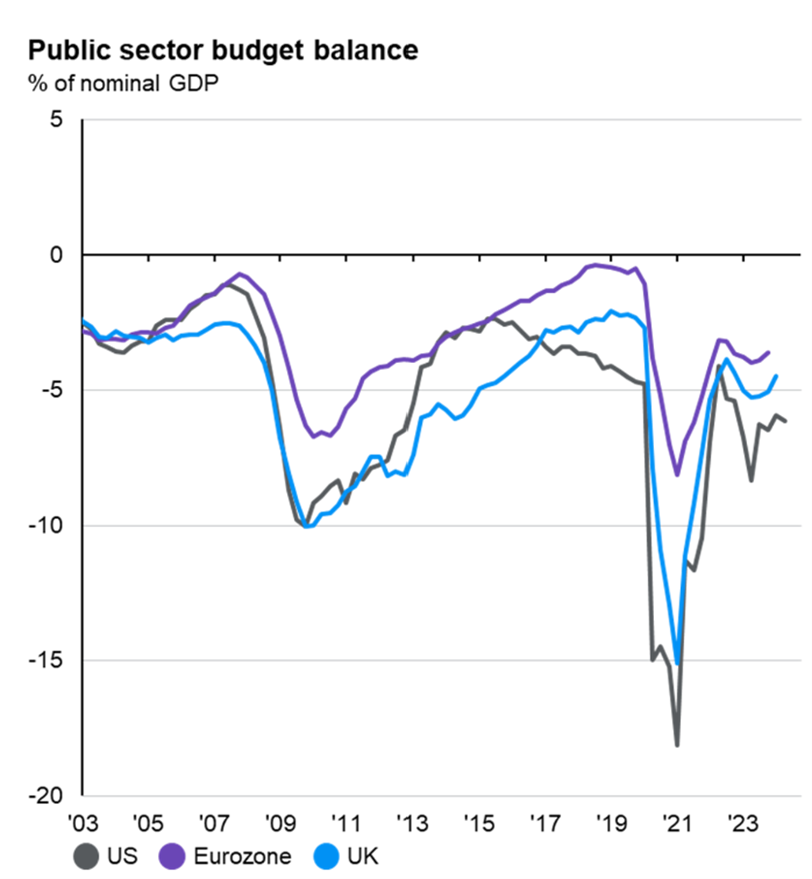

The rather mundane answer is: ‘not an awful lot’. When the election got announced, UK Equity and Bond markets barely reacted. Labour was then so far ahead in the polls that a Labour victory seemed a foregone conclusion meaning markets would have already been pricing in this result. It is therefore no surprise that at the time of writing, about midday the day after the election, the FTSE 100 is completely flat. Governments around the world at the moment are running rather hefty budget deficits including the UK (as shown in the image below). With interest rates as high as they are, the ridiculous amount of money that the UK Government has to spend on interest payments alone, mean that whichever party is in power, has very limited fiscal headroom.

Source: JPM Guide to the Markets

Governments, can of course, sideline the Office for Budget Responsibility, as Liz Truss did and break their self-imposed fiscal rules, but I think Truss’ catastrophic budget serves as a painful reminder of what’s at the end of that path. Furthermore, they have pledged to include a forecast from the Office for Budget Responsibility in their next budget and Labour’s main priority is to provide economic stability – so I think we’re safe on that front, although the same can’t necessarily be said for the French (more on that next week). It will continue to be economics not politics that drive UK Equity markets, as inflation looks to be almost under control and interest rate cuts loom.

So how will Labour achieve their priorities?

Paying staff more at the NHS to cut wait times, more police and more teachers all cost money – more money than Labour can spend. This means that they will have to increase their revenue i.e. raise taxes. Starmer has been very clear on not increasing income tax rates, National Insurance or VAT. We don’t want to speculate too much on tax, but that does leave Capital Gains Tax awfully vulnerable. Other areas that haven’t been ruled out are pensions and inheritance tax. Coming at it from an investment perspective, I think the only implications here are for the AIM market, a UK small cap index, of which many shares qualify for Business Property Relief (if you hold them for 2 years they are outside of your estate). If Labour were to scrap BPR or reduce its effectiveness, this could have serious implications on AIM and is something we’re actively discussing at Bowmore.

Despite Keir Starmer proclaiming this morning that ‘the work of change begins immediately’, it’ll be some time before we see any actual change. There is no date for the next budget and any changes we see, like an increase in Capital Gains Tax rates, will likely not come into effect immediately but rather at the start of the next tax year. In summary, we should hopefully have a period of stability in UK Equity and Bond markets, at least in the short term.